Attention Self-Funded/Level-Funded Small Employers under 50 employees

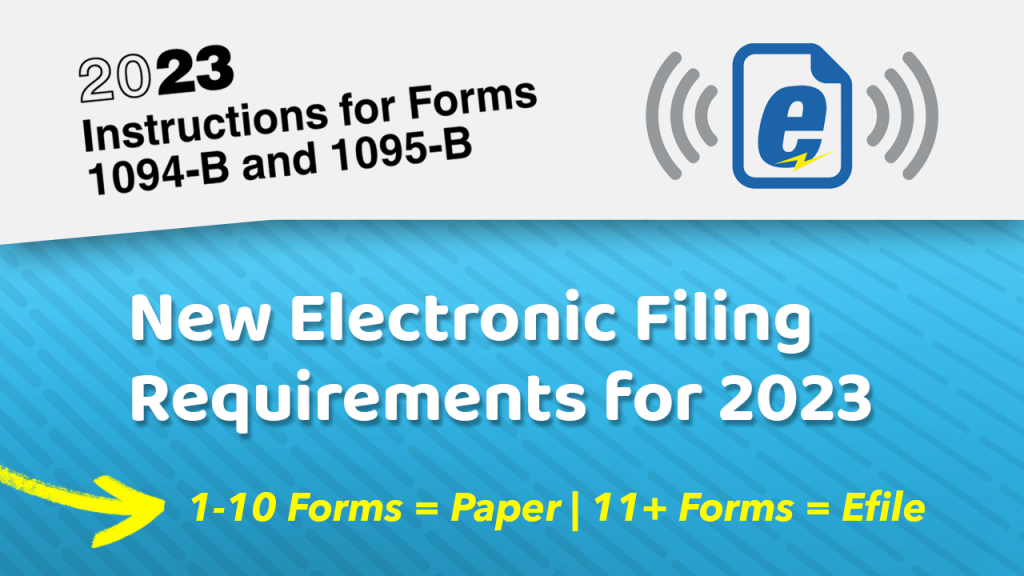

Electronic Filing: Previously, employers had the option to submit their ACA reporting forms on paper if their total filings numbered fewer than 250. However, starting in 2024, employers who submit more than 10 returns collectively are mandated to file electronically. This effectively eliminates the paper filing option for almost all employers, unless they are granted an exemption due to hardship.

Deadlines: Employers are required to file to the IRS by April 1, 2024 when filing electronically. Additionally, employers must provide the relevant Form 1095-B or 1095-C to their eligible employees by March 1, 2024. The deadline for furnishing Form 1095-B/1095-C has been automatically extended from January 31, 2024, to March 1, 2024, with no further extensions granted.

Electronic Filing Waiver: Employers have the option to petition for a waiver from the mandatory electronic filing if they can demonstrate that electronic filing would pose an undue hardship or conflict with religious beliefs. Requests for waivers must be submitted at least 45 days before the return due date, but no later than the due date itself. Waiver requests utilize Form 8508, Application for a Waiver from Electronic Filing of Information Returns. First-time waiver applicants for any of the specified forms will automatically receive approval. If citing undue financial hardship, the applicant must obtain current cost estimates from two service bureaus or third parties and include them with Form 8508.

Penalties: Failure to file electronically when required, without an approved waiver, may result in a penalty of $310 per return, unless reasonable cause can be established. The penalty for failure to file a correct information return is $310 per return, not exceeding $3,783,000 in total for a calendar year. Similarly, the penalty for failure to provide a correct payee statement is $310 per statement, not exceeding $3,783,000 in total for a calendar year.